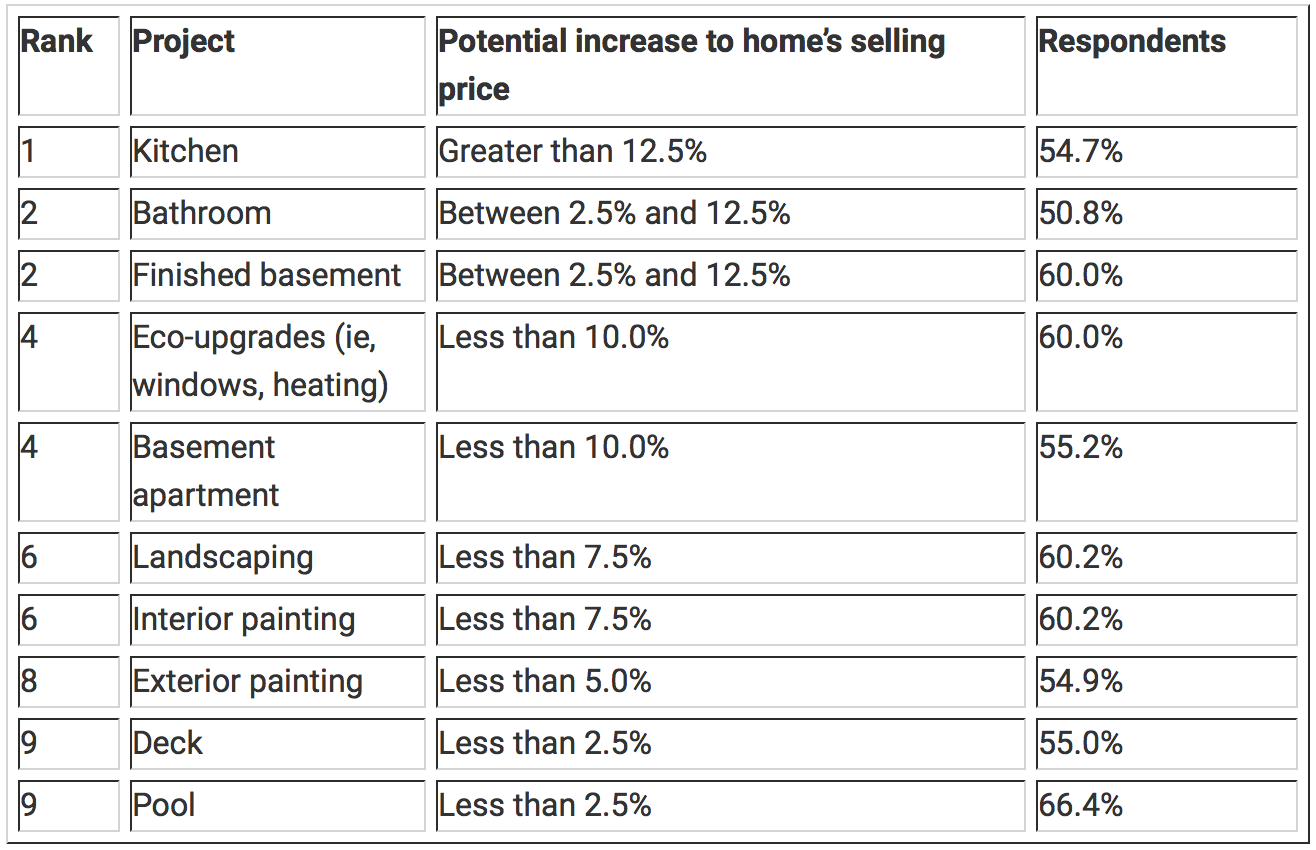

TORONTO, JUNE 28, 2018 – According to a cross-Canada survey of over 750 Royal LePage real estate experts, a kitchen renovation is the clear upgrade of choice with the potential to boost a property’s value by more than 12.5 per cent.[1] Both ranking second, a finished basement or a new bathroom has the potential to increase a property’s value between 2.5 per cent and 12.5 per cent, depending on the investment.

“To financially benefit from a home improvement project, you need to keep potential homebuyers in mind,” said Tom Storey, real estate agent, Royal LePage Signature Realty. “While updating a kitchen should increase your sale price, a pool can actually deter families with young children or those who are looking for less maintenance.”

Adding a pool or deck is considered the least worthwhile renovation to increase a property’s value with pricing potential limited to a maximum of 2.5 per cent of the value of the home.

For Canadians looking for more general guidance on where to focus their home projects, the vast majority of surveyed experts recommended interior renovations (95.0%) over exterior renovations (5.0%).

“Curb appeal is important but more time is spent indoors at the open house and that is where buyers typically fall in love with a home,” added Storey. “When renovating with the potential to sell, the most important thing to remember is to use colours and materials that are popular and not too personal.”

The survey showed that prospective sellers are willing to invest less than 2.5 per cent of a property’s value on home renovations prior to listing their home, which represents an investment of up to $15,138 on a property valued at $605,512[2] – the current median home price in Canada.

When asked which generation is the most likely to renovate their home, 45.1 per cent of surveyed experts said baby boomers, as many are planning to sell and downsize. They are also most likely to have the funds needed for a significant renovation.

“Baby boomers run the risk of their property selling for a lower price or languishing on the market for longer than expected if they held their property for a long period of time without updating periodically,” said Storey. “Although many buyers can see themselves making home improvements themselves, its very hard for a buyer to get excited or imagine living in a space that is run down or the decor reflects another generation.”

Popular Home Improvements

About the home renovations ROI survey.

The Royal LePage Home Improvement Survey polled 766 real estate advisors from across Canada, between June 20, 2018 and June 25, 2018. Each respondent was asked to complete an online survey composed of 8 questions on the value of popular home improvements.

[1] Statistic referenced in table Popular Home Improvements

[2] National Home Price Aggregate, Royal LePage House Price Composite, Q1 2018.

This article is curtesy of www.royallepage.ca.

I offer complimentary home evaluations. Please do not feel obliged to list and sell with me when you request your current home evaluation. I am always happy to help, and when you are ready, I will be available to provide you with my full real estate experience.

Request your home evaluation:

PLEASE CALL/TEXT AT 416-419-5226 OR EMAIL LUBA@LUBABELEY.COM

![Hotel Mono is All Monochrome [Singapore]](https://images.squarespace-cdn.com/content/v1/58ce8b4db3db2b938eb31992/1498245340339-FKZBVE33NCF7287LT9AH/hotel-facade.jpg)

![The Whitby Hotel [New York] - WOW!](https://images.squarespace-cdn.com/content/v1/58ce8b4db3db2b938eb31992/1498234292888-ROPKOHVVVEQBTBIJ6EPP/whitby-hotel-new-york.jpg)